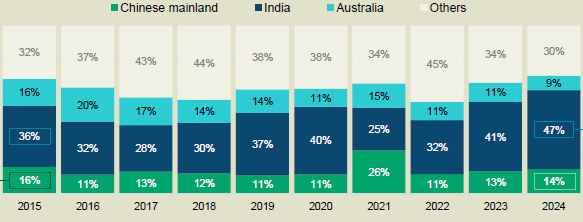

Knight Frank, in its newly released Asia-Pacific Horizon II report titled Whiplash to Resilience: Corporate Real Estate in the New World Order, highlights India’s growing dominance in the regional office leasing market. In 2024, India accounted for 47% of all APAC office leasing volumes, up from 36% in 2015, underlining its strategic relevance amid trade shifts, supply chain diversification, and macroeconomic headwinds.

India’s office transaction volumes reached a record 6.68 mn sq m (7.19 mn sq ft) in 2024, led by robust demand from Global Capability Centres (GCCs), multinational occupiers, and third-party IT service providers. The report positions India as a long-term, stable hub for occupiers seeking cost efficiencies, talent depth, and infrastructure readiness, particularly in cities such as Bengaluru, Hyderabad, Pune, and NCR.

Office leasing volumes pivoting toward India

Source: Knight Frank Research

Shishir Baijal, Chairman and Managing Director, Knight Frank India, said, “India’s share of Asia-Pacific’s office leasing volumes rising to 47% is a testament to the country’s robust fundamentals and growing appeal as a strategic hub for global corporations. With the rapid evolution of India’s services and manufacturing ecosystems, the country is increasingly seen as a stable and scalable alternative for long-term investments. As global corporates seek operational resilience amid ongoing trade realignments, India’s real estate sector stands well-positioned to play a pivotal role in the regional growth narrative.”

|

Industrial Market Stability |

While several APAC markets face oversupply challenges (Shanghai, Beijing), Indian industrial hubs such as Mumbai, NCR, and Bengaluru have maintained balanced vacancy levels, backed by sustained leasing activity.

The report notes that build-to-suit formats and flex leases are gaining traction in India, reflecting a shift toward customisation and operational agility.

|

India’s Resilience in the Vulnerability Matrix |

India sits in the ‘low exposure, moderate resilience’ quadrant. This indicates relatively low external trade dependence and a strong ability to absorb global shocks. In contrast to export-heavy economies like South Korea or Singapore, India’s large domestic consumption base, prudent fiscal management, and diversified services sector buffer it against external volatility—making it a reliable anchor in the region.

Vulnerability Matrix

|

Regional Realignment and Growth Hotspots |

The report outlines a significant shift in regional investment and occupier focus driven by the Trump 2.0 tariff regime and reconfiguration of global trade lanes. Southeast Asian markets such as Vietnam and Indonesia are expected to see 15–20% growth in demand for industrial space due to increased manufacturing interest. However, India stands out in office leasing, absorbing nearly half of all APAC leasing volume—a testament to its leadership in the services-driven economy.

Meanwhile, flexible leasing formats, build-to-suit preferences, and portfolio optimisation continue to shape occupier strategies across APAC. India has been early to adopt such trends, with strong traction in flex space leasing, particularly from tech firms and start-ups seeking agility and cost control.

|

A Pivotal Role Ahead |

India’s consistent performance is underpinned by rising domestic demand, digital transformation, and supply-side readiness across Grade A commercial assets. While global headwinds persist, India’s positioning as both a growth engine and a resilience play makes it central to CRE strategies across Asia-Pacific.

As businesses recalibrate real estate portfolios to withstand volatility and tap new markets, India’s evolving real estate landscape offers both scale and stability—cementing its role as a cornerstone of APAC’s corporate property narrative.

Tim Armstrong, Global Head, Occupier Strategy and Solutions, Knight Frank, says, “Our analysis shows that while the temporary tariff reduction provides companies with breathing room, the 'China+N' strategy has become a standard operating model rather than just a response to tariffs. We have entered a time where corporate real estate strategy must evolve from footprint expansion to operational durability and total-cost performance. This isn't a cyclical adjustment, it's a structural transformation that requires entirely new approaches to portfolio planning, lease structures, and location strategy.”